Cutera Writeup

Revolutionary new medical device + world-class management team = superior shareholder returns.

Thesis:

Cutera provides the opportunity to invest in both a revolutionary new health device and alongside world-class capital allocators. Cutera’s recent introduction of Aviclear will revolutionize acne treatment. Cutera's new CEO, Taylor Harris, is a seasoned medtech veteran with a history of exceptional shareholder returns. Despite these positive developments, investors have abandoned the stock due to prior executive drama that temporarily paralyzed the company. I believe the shares can ~14x over the next three years.

Business Overview:

Cutera is a medical aesthetics company that sells laser and RF technology products for a variety of skin revitalization, body contouring, hair, and tattoo removal uses. Cutera primarily sells its technology to plastic surgeons, dermatologists, and other licensed physicians.

In 2015, Cutera pivoted away from cyclical capital sales to a more stable recurring revenue model. From 2015 onward, Cutera only released products that had a consumable element, thus creating a stream of recurring revenue even after an initial capital sale occurred. Today, recurring revenue comprises 35% of total sales with management targeting 60% recurring by 2026.

Aviclear Opportunity

In March 2022, Cutera received FDA approval for its Aviclear device, which is a 1726 nm laser used to treat acne. Unlike other laser devices, Aviclear’s laser treatment directly attacks the sebum glands responsible for producing acne. In three quick thirty-minute sessions across two months, Aviclear was found to improve skin in 90% of patients.

Aviclear’s initial customer reviews have been phenomenal. On the cosmetic review site RealSelf, Aviclear has an 88% “worth it rating”, already making it one of the top-rated Acne treatments. Here are some of the positive reviews:

“I've posted a ton of super vulnerable pics below for the whole world to see my skin healing journey. AviClear is worth every penny. I spent $2500 (the cost would've been $3K, but my provider gave me a $500 discount). I've spent THOUSANDS of dollars on skin care, facials, other lasers that just did more damage, harmful oral medications like spironolactone and minocycline and those never worked. Don't take those meds, especially ACCUTANE! They will damage your liver and cause severe joint pain and other long term effects. I hope AviClear shuts those companies down or at least gives them a run for their money because there is little to almost no side effects with AviClear.”

“I have struggled with mild to moderate acne and oily skin for about 10 years now, and after receiving my three aviclear treatments, I can already see a difference…”I am almost 2 months out from my last treatment, and I can already tell a difference.”

“Aviclear changed the game for me, I feel normal again and for the first time in years, I feel beautiful. I did purge after the first and second treatment but I noticed my breakouts weren’t lasting as long as usual. Since my 3rd treatment I have only had 3 pimples. The treatment can be a bit uncomfortable depending on your pain tolerance. But I would do it every month for the rest of my life for these results.”

As part of my research, I also spoke to the owner of a dermatology practice. They raved about Aviclear’s proprietary technology, effectiveness, and minimal side effects. The owner would go on to say:

“Nobody has a laser device that can treat acne the same way.”

Aviclear comes with unique unit economics. Instead of selling the system outright, Cutera leases it to physicians for $5,000 a year. On top of this annual fee, Cutera collects $1,500 for every procedure done using Aviclear. While this may seem steep, physicians typically charge $3,000+ for an Aviclear treatment. Physicians also prefer leasing Aviclear for 5,000 a year as it’s far cheaper than buying the system outright.

Aviclear’s annual lease and procedure payments create a steady stream of recurring revenue for Cutera. While Aviclear is currently running at a loss due to initial investments in sales and marketing, management believes Aviclear’s long-term gross margins will approximate 70-75%. If they’re right, Aviclear could easily generate operating margins north of 20-25%+, assuming SG&A and R&D make up 50% of sales.1

Aviclear’s TAM is enormous–and likely understated. 6.5M Americans seek clinical acne treatment every year. Accutane is the most popular treatment, which is prescribed to 400,000 patients annually. Accutane is a once-daily pill that increases the shedding of dead skin cells and thus reduces pore clogging. Patients are usually on the drug for four to six months. Similar to Aviclear, Accutane has a ~ 90% efficacy rate.

Accutane, however, comes with numerous restrictions. Patients on the drug are not permitted to drink alcohol and must use birth control. Female users have to submit a negative pregnancy test each month to refill their prescription. Considering the average patient is a woman in their twenties/thirties, these restrictions are especially burdensome and likely deter many would-be users.

Aviclear has none of Accuitane’s limitations. Instead of being a six-month regime, patients are treated in three quick thirty-minute sessions across two months. There are no restrictions regarding alcohol consumption or birth control. Aviclear also has minimal side effects. I see Aviclear as a TAM expander because of these reasons, with more patients seeking out Acne treatment than ever before.

Why Does This Opportunity Exist?

Investors have orphaned Cutera equity due to epic drama in the C-suite. Here is a quick timeline of events:

· April 7th: Executive Chairman Daniel Plants and CEO Dave Mowry demand a special board meeting to remove five board members over their failure to create a proper succession plan for Mowry. The board of directors forms a special committee to consider their proposal.

· April 11th: A group of Cutera executives issued a letter asking that the dispute be resolved quickly so it doesn’t harm Cutera’s business.

· April 12: The board of directors fires Plants and Mowry and appoints current board member, Sheila A. Hopkins, to serve as Interim CEO. The board initiates a search for a new permanent CEO and pulls annual guidance. In the press release, the board reveals that former Chairman Plants had attempted to fire former CEO Dave Mowry in November 2022 and February 2021.

· April 17th: The board of directors writes a letter to shareholders, detailing its rationale for removing Plant and Mowry. The board did not believe Mowry was the right leader for launching Aviclear nationwide and revealed Plants had been trying to name himself CEO in place of Mowry. The directors ask that shareholders do not vote in favor of Mowry’s proxy.

· April 24th: The Special Committee releases a letter supporting the new interim CEO and current board of directors.

· May 9th: Rohan Seth, Cutera’s CFO, resigns from his position effective immediately. Seth’s resignation was not due to any disagreement with the company or the board of directors. Stuart Drummond is named interim CFO in his place

· May 10th 2023: Cutera’s Q1 2023 earnings are released. The stock fell 12% as interim management refused to put out annual guidance.

· May 19th: The board of directors temporarily expands to 11, as four new members join the board. All four new board members possess decades of experience in the Medtech and aesthetics industries and will aid with the search for a new CEO

· July 27th: Cutera announces Taylor Harris as their new CEO. Harris was one of the four temporary board members appointed in May.

While it may be difficult to comprehend at first glance, I believe the board was justified in removing Mowry and Plants. As CEO, Mowry botched the roll-out of Aviclear nationwide by failing to meet initial guidance while simultaneously cannibalizing sales in Cutera’s other lines of business.

Plants, on the other hand, was competent but with malevolent intentions: He was more concerned about becoming CEO and using the company as his personal enrichment vehicle. Looking back, Plants’ end game after teaming up with Mowry was clear: Take control of the board, appoint new board members favorable to him, vote himself new CEO, and either take the company private at a price far below intrinsic value or pay himself a lavish salary as CEO. Either scenario would have been disastrous for Cutera shareholders.

Between April 7th and today, Cutera stock has fallen from $23 to ~$3 a share. I believe investors have puked the stock due to the outlandish C-suite drama Former chairman Plants also likely exerted heavy selling pressure on the stock as he exited his 7% ownership stake through his hedge fund.

Management: World Class Capital Allocators

In the end, Taylor Harris being appointed CEO will significantly strengthen Cutera’s business. Harris previously served as the CFO of three different publicly traded Medtech companies: Myokardia, Zeltiq, and Thoratec. During his first earnings call, Harris confirmed that Cutera’s issues are both temporary and fixable:

“They're not --these are not technology issues, these aren't clinical data issues, these are execution issues. And so we just need to focus on them. And so, all of that made me feel excited. I'm here not for a couple of quarters but, for a long time, and we're going to start working on it right now.”

Later in the call, Harris would name three key initiatives he wanted to improve as CEO:

· Improve reliability and quality issues

· Educate physicians to turn Aviclear placements into more procedures

· Refocus on core capital business

Harris has already beefed up Cutera’s operations by hiring former Zeltiq executive Brent Hauser for Aviclear’s international expansion and seasoned Medtech vet Jeff Jones as chief operating officer.

I also believe that Harris will right-size Cutera’s bloated cost structure. Cutera spends $162M on SG&A–or an eye-watering 62% of sales! For reference, Inmode, Cutera’s closest public comp, SG&A spend is 38% of sales. Cutera employs 540 full-time employees. Inmode, which has twice as many sales as Cutera, has just 480 employees. There’s clearly a lot of room for trimming operational fat to improve profitability.

Furthermore, Harris’s incentive package as CEO is well-aligned with shareholders. Upon his hiring, He was awarded over 250,000 RSU that began vesting at $20, $25, $30, and $35 a share. If successful in hitting all those milestones, Harris stands to make $6.75M, or about 10x his annual base salary. Harris also purchased $350K worth of Cutera stock on the open market at the end of August for $9 a share. The $350K investment represented half of Harris’s base salary.

Finally, it's important to note all three of Harris’s former employer's companies would later be acquired for significant premiums under his tenure:2

Cutera has been the subject of M&A rumors for the better part of a decade. Given Harris’s previous experience, a sale of Cutera seems like the foregone conclusion of his turnaround plan.

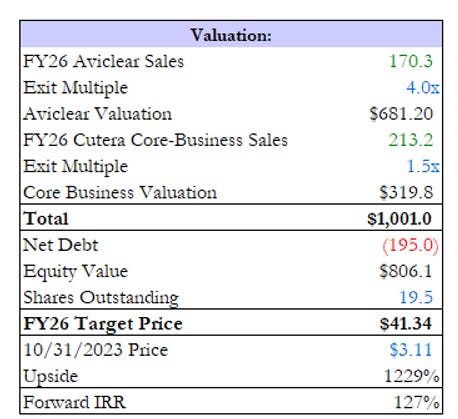

· Valuation:

For modeling here's my base scenario:

AviClear System adds 1,000 new systems in FY23 and 1,200 each year until FY26. Based on my primary research, each system is expected to treat 30-50 patients annually. For conservatism, I assume a slow ramp-up from 3.5 to 18.5 patients a year, with each system adding five patients a year through FY26. Taking it together, I get total Aviclear sales of $170M in FY26:

What would the market be willing to pay for a Medtech company growing sales by 70% with a highly recurring revenue base and gross margins of 70-75%? I’m not sure precisely but 4x sales seems like a nice conservative exit multiple. That gets me to $680m in value for Aviclear.

What about the rest of Cutera’s core business? My base case is as follows:

System North America: Down 15% in 2023, Returns to 4% growth in 2024 and beyond in line with pre-covid trends.

ROTW Systems: Up 12% in 2034 in line with the prior two quarters. Growing 5% in 2024 beyond in line with pre-covid trends.

Consumables: Growing 12% over the projected period

Service: Growing 2% over the projected period

In all, I get FY26 revenue of $215M:

Inmode, Cutera’s closest public comp, trades for about 2.5 sales. For conservatism, let’s say Cutera's core business is worth 1.5x sales, which gets me to $319M in value. Adding this with my Aviclear valuation and Cutera’s enterprise value is ~$1B. Subtracting Cutera’s current net debt position of $195M, I get $805M in equity-or about $41 a share, which represents a 14x from current prices:

Cutera’s leverage is the biggest risk to my forecast. The company currently has a debt position of $410M against $225M in cash. Based on Q2, Cutera will burn another $70M by year-end, giving it $150M in cash. All of this debt, however, is in convertible notes with reasonable coupon payments, which don’t start maturing until 2026 at the earliest. This hopefully gives Harris plenty of time to turn Cutera cash-flow positive and either refinance with a new convert or pay with cash on hand.

Risks:

o Recession: Aviclear and many of Cutera’s other products are not covered by insurance, thus making it sensitive to any sort of pullback in consumer spending.

o Execution: Harris’s past track record is not a guarantee of future success. Cutera’s business model might be broken for good, despite Harrs’s best efforts.

o Competition: Other aesthetic companies could produce their version of Aviclear and thus compete with Cutera.

o Financing: As mentioned above, Cutera is saddled with a decent amount of debt and is neither cash flow positive nor profitable. Failing to repay the debt would significantly impair Cutera’s equity.

Conclusion:

I’m only going to invest $4,500 for now. While I feel confident in my forecast of the business and my read-on management, there are numerous overhangs here between cleaning up Cutera operationally, leverage, and restarting Aviclear’s commercial rollout. Until then, I’ll be carefully watching to see if Cutera is on track to turn cash flow positive/profitable, ensuring the debt can be repaid. Once these risks have been addressed, I’ll be more than happy to add more (albeit at higher prices) and make it more of a core position.

I bought 1,475 shares at $3.05 a share.

-Seldon:

Inmode, Cutera’s closest public comp, spends 48% of sales on SG&A and R&D.

Starting approximate price when Harris was named CFO. IRR=Return from when Harris became CFO to the day of buyout was announced.

Thanks for the write-up. Some things that popped in my mind when I read the thesis:

* On what basis are you assuming they will add 1000 systems FY23 and 1200 in the upcoming years? Also, according to the license revenue projection from FY23 and onwards, it assumes that all of the added systems are installed and accounted for from first day of the year. A more realistic scenario is that they install some continuously, which would add some latency to the revenue. But I assume you purposely modeled as you did for simplicity.

* There only seem to be 1 valid paper about this device https://pubmed.ncbi.nlm.nih.gov/36576854/

However majority of the authors are associated with Cutera, and the whole study only includes 14 test subjects. So there is a risk this paper is funded and biased by the company itself to make it look better on the surface. They could have purposely chosen their subjects with the highest probability to yield good results by chosing people with certain ethincity, skin-type, etc.

* The " Accutane has a ~ 90% efficacy rate. " statement should be taken with caution. How many test subjects is this based on, who presented this number (if it is from the company itself, do not count it as unbiased), etc...

* "Aviclear has an 88% “worth it rating”, " This number is based on 80 reviews, which is a bit low IMO. Also, I'm not sure how reliable and unbiased these reviews are. Perhaps they don't represent the real "worth rating" accurately since these reviews could just be made by the company more or less. But I could be wrong here since I do not know much about this webpage

* I don't quite follow how you calculate fee revenues? Also what do you mean when you first state 30-50 patients are treated per year, but then 3.5 patients per year? 3.5 + 30-50 ? I am just a bit confused here :)

* With all this said, say the product only turns out to be an "OK" which mostly works but not as effective as they portray it to be, leading to a bit more conservative values where it takes longer time for people to accept it as a legit replacement to antibiotics and other treatments (IMO more realistic). Say we have 3.5 FY23 to 6 FY26 patients a year with only 600 newly placed systems per year as the first year, what value would you get instead with your multiples?

Thanks

/O

What’s your feelings about this past weeks earnings?