MODG Long Thesis

"TopGolf is the greatest thing to happen to golf since Tiger Woods"-MODG CEO

Thesis:

TopGolf Callaway is a dominant entertainment franchise that is trading for just 11x EV/EBITDA. Despite high levels of growth reinvestment, the TopGolf segment is poised to become cash flow positive this year, with the potential to generate hundreds of millions in free cash flow for years to come. I believe MODG could generate $470M in free cash flow in 2026, hitting $37 a share or an upside of ~85%.

Business Overview:

TopGolf Callaway is a market leader in the golfing industry. For the company’s first 35 years of operation, it only sold golf clubs and balls. Over the past five years, Callaway has expanded into the apparel business with the acquisition of OGIO in 2017 for $125M and Jack Wolfskin for $475M in 2019. In October 2020, Callaway made its most transformative acquisition yet, purchasing TopGolf for $2B.

Today, revenue is split into three segments:

TopGolf (2022 FY sales of $1.5B or 45% of total sales): A unique golf entertainment franchise with over 80 locations in the United States as of FY22. 33% of sales are from bay bookings, 33% from food & beverage, and 30% from events.

Golf Equipment & Balls: (2022 FY sales of $1.4B or 35% of total sales): Selling golf balls, clubs, putters, and bags under the Callaway and Odyssey brand.

Apparel (2022 FY sales of $1B or 20% of total Sales): Sells clothes, jackets, backpackers, hats, and other apparel under the OGIO, Jack Wolfskin, and Travis Matthew Brand.

TopGolf: A Unique and Dominant Entertainment Franchise

TopGolf was founded in 1997 by two brothers from outside of London, who were bored with the traditional driving range experience. The pair developed a unique tracing technology that enabled golfers to see each ball's distance, trajectory, speed, and flight path. Topgolf’s first range was opened in 2000 in Watford, England. Initially, the venue was just a driving range with high-tech tracking equipment. It was not a financial success. After consultation from an outside investor, the brothers redesigned their original venue to be multi-storied and include a full-service kitchen. TopGolf then went across the pond to test this new design in US markets. After a couple of tries, the brothers had found their groove with their first opening in Dallas, with wait times hitting six hours in less than a year. Today, TopGolf has over 80 locations across the US.

Unless you’ve visited one before, it’s difficult to explain TopGolf’s magnitude and unique experience. It truly is a one-of-a-kind entertainment asset.

Each bay has a full set of golf clubs (sans putter), two TVs, and enough seating and tables for 6-10 guests. You're not driving into an empty field when you hit the ball into the range, like at your average golf course. Instead, the range has over ten different targets, which are giant nets ranging from 10-50 yards in diameter. The nets are then segmented into 3-5 circular compartments, expanding as you get farther away from the center. You get more “points” for hitting the ball into farther nets and closer to the center.

In 2021, TopGolf registered thirty million unique visitors. Despite golf’s elitist reputation, 51% of visitors were non-golfers. After one round at TopGolf, 75% of these non-players express interest in picking up golf. That equates to over 11M potential new golfers each year! In other words, Topgolf has become the greatest customer acquisition funnel for golf since a kid from Orange County made shots like this look easy.

TopGolf’s operating model is not easily replicable. For starters, each venue occupies an average of 65,000 square feet! This isn’t a QSR concept that can be plopped down on any random vacant commercial lot. Building a new venue can take between 10-15 months. Construction costs range between $10-$55M. In a rare instance of clever financial engineering, Callaway sidesteps the massive investment by having the REIT, the owner of the land, reimburse 75% of construction costs. Landlords agree to this deal as TopGolf venues has proven unit economics that will provide a steady stream of rent upon completion. On top of this, a competitor would need to develop their own tracing technology for the golf balls. All in all, you’re looking at investing close to tens of millions before your first customer ever hits a ball.

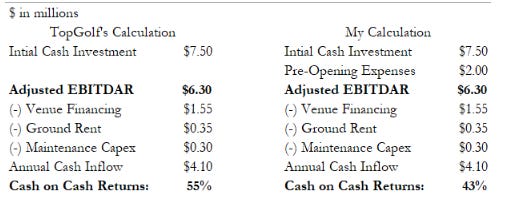

Once constructed and open to the public, TopGolf venues have highly attractive financial returns:

The most important metric here is cash-on-cash returns. For non-real estate investors, cash on cash returns equates to return on invested capital in equities: it represents the cash flow received relative to cash invested in a property. Earning 8-12% is perceived as a “good” return in the real estate world. Getting 50-60% on one investment, let alone dozens of them, is unheard of. However, I estimate cash on cash returns are closer to ~40%.

My calculation includes pre-opening costs (employee recruitment, training, initial marketing, etc). Callaway excludes them. To me, this seems like a “real” cash outlay. Regardless, a 43% cash-on-cash return is still a phenomenal ROI.

Further highlighting Topgolf’s fantastic unit economics, management has raised target venue margins and cash-on-cash returns twice already since acquiring Topgolf. During the M&A call, management guided toward a 31% EBITDAR venue margins and 30-40% cash on cash returns. Eighteen months later, they raised their target for 33% margins and 40-50% investment returns. These past earnings they once were against raised their target. This time for 35% EBITDAR margins and 50-60% cash on cash returns.

There is evidence to suggest there is further room for improvement. As it stands, average utilization each week (measured by the percentage of bays occupied) stands at only 40%. On the weekend, utilization climbs to 70%. Good, but nowhere near full capacity.

Venues are experimenting with a new digital booking system to further improve utilization. Called PIE, the new system enables customers to book bay in advance online instead of through walk-ins. PIE has already rolled out to 30 venues with plans to expand to all US venues by the end of 2023. Venues with PIE are already seeing a 2% lift in sales. With the new system, management is aiming for half of the bookings to be done online, compared to 30% currently.

In the future, PIE could be further leveraged to create a “dynamic” pricing system. Based on past booking data, venues could lower prices on the weekdays, enticing customers to visit earlier in the week rather than on the weekend. The incremental customer visits during these typically slow times could further enhance venue-level unit economics.

TopGolf also has plenty of pricing power to raise bay prices during busy times. On the weekend, wait times at venues often exceed 2+ hours. TopGolf could easily do surcharge pricing during these busy times, further boosting profits.

As of writing, there are ~83 TopGolf venues in the United States. Management believes the country could support 250 locations. While these entertainment venues may seem ubiquities in urban centers, much of the country lives nowhere close to a location. According to internal metrics, only 25% of the population lives within 25 minutes of TopGolf. That leaves nearly 250M Americans without easy access to a TopGolf. Expanding to 250 locations doesn’t appear to risk oversaturation knowing this. And perhaps, like other financial metrics, management is lowballing TAM and it’s closer to 300. Either way 250 venues nationwide seem like a reasonable long-term aspiration.

Management aims to open 11 new venues a year. As illustrated above, construction is a capital-intensive process. I estimate Callaway has spent $1.26B on growth capex in the last three years. The heavy investment has eaten up all the operating cash flow and then some. The good news is that TopGolf is not only on-pace to become self-funded this year but also that MODG is slated to turn positive cash flow. This should alleviate investors’ concern about TopGolf’s true profitability. Furthermore, management guided towards annual TopGolf capex normalizing around $200M. If existing TopGolf venues can achieve target unit economics along with the apparel and equipment segments remaining profitable, MODG should just gush cashflow with just $200M in capex.

Investors are skeptical. The stock is down 10% since the last earnings report, despite raising guidance and TopGolf unit economics. In other words, this is a “show” me story. I’m willing to take a leap of faith given management’s prior history of shareholder value creation:

Management:

TopGolf Callaway is led by CEO Oliver “Chip” Brewer. Before Brewer became CEO, Callaway had four different CEOs in 11 years, with the last not even being a golfer! During this period, the stock underperformed the S&P 500 by 200%. Chip righted the ship by selling off underperforming brands like TopFlite and Ben Hogan in his first year. Since then, Callaway's stock has more than tripled. The S&P 500 is up just 210% during the same period.

Before Callaway, Chip served as CEO of Adams Golf for ten years. During his tenure, Adams Golf stock went from $2 to $10 a share, before being sold to TaylorMade. Brewer also has a history of strong capital allocation through M&A with the Jack Wolfskin and Travis Matthews acquisition. Before acquiring a majority stake in TopGolf, Brewer had made multiple investments in Topgolf as early as 2006.

Today, Brewer owns ~$25M worth of stock, or 25x his base salary. Another board member, Thomas G. Dundon, owns 10% of common stock outstanding through his investment firm, DDFS investment management (shares acquired during the TopGolf merger). Together, these two individuals account for nearly all the insider ownership (~11% in all). Four different directors/executives, including Brewer, have also purchased $100,000 or more of shares on the open market in the past year. Insider buying was strongest after the Q1 earnings sell-off, highlighting insider’s confidence.

Valuation:

Despite its straightforward business model, valuing MODG proved to be quite difficult. There are many moving parts and insufficient transparency to create precise forecasts. As a result, I had to keep my valuation simple. Here are my assumptions:

TopGolf will have 92 domestic venues by FY2023. All of these venues reach maturity by FY 2026, with each generating $3.4M in free cash flow, which is in line with the venue unit economics described above.

Both apparel and golf equipment grow 3% annually from now until 2026 with a 6% free cash flow margin, which is consistent with the performance of these brands from 2017-2019.

Cumulatively, this equates to $472M in free cash flow, which divided by 200M shares outstanding equals $2.36 in free cash flow per share.

Applying a 16x multiple, or about a market multiple, I get a share price of ~$37, or 85% higher than current levels.

Ultimately, these assumptions are uber-conservative. I prescribe no incremental revenue or cash flow from TopGolf opening additional venues from now until 2026. My growth estimates for apparel and golf equipment are also likely lowballed, considering both segments grew 10%+ in Q1 2023. Nevertheless, caution is warranted given the uncertain macro environment (golf spending is cyclical) and the fact that current disclosures limit precision.

Some extraneous call options:

Embedded in our Topgolf investment are a few call options that can further enhance our IRR. For the sake of conservatism (and complexity!), I haven’t included any of these aspirations in our final model.

Top Tracer: TopTracer is a capital-light and high-margin analytics platform. It provides instant data and flight civilization of hit balls. In 2019, TopGolf began selling this technology to ranges in the form of hardware and subscription. Once installed, golfers flock to ranges that have this technology as it provides instant feedback for every shot hit. In some instances, venues that install the technology see revenue increase by as much as 25-60%!

Management believes they can sell the technology to over 600,000 individuals driving bays globally. They have currently penetrated less than 5% of that figure. Each bay provides $2,000 in sales and $1500 in AEBITDA each year. Not too shabby. Management believes the long-term earning power from the TopTracer segment could be as high as $200M in AEBITDA.

International Venues: Management believes ROTW (outside the US) could support an additional 200 TopGolfs. As they expand abroad, management has decided to franchise these operations instead of owning them outright. Assuming a 6% annual royalty rate and $17.5 sales per venue, 200 international revenues could provide MODG $210M in annual revenue, which paired with an 80% EBITDA margin, could add $170M in high margin recurring annual EBITDA.

Travis Matthew: Travis Matthew is one of the apparel brands Callaway acquired in 2017 from OGIO. Today, the brand does $300M in sales and $50M in EBITDA. Management is aiming to get $500M of sales by 2025 and sees a path to $1B. My sum of parts analysis suggests that Travis Matthew could easily be worth >$1B if MODG can hit these goals.

Risk:

Recession Risk: Despite its older and wealthier demographic, golf is sensitive to economic downturns. In 2008 and 2000, golf spending fell in the high single digits.

Leverage Risk: MODG is highly levered with 4.5x Debt to EBITDA. Rising interest rates could impair our investment or force management to curb TopGolf expansion plans.

Disclosure Risk: This pertains to our investment thesis, not the business. MODG doesn’t do a good enough job of disclosing all the portions of their business, leaving investors in the dark. For example, there’s no disclosure around TopTracer regarding the exact number of bays, revenue, or AEBITDA. The apparel segment has no discretion between Travis Matthew and Jack Wolfskin.

Even the firm’s crown jewel, TopGolf, doesn’t break out unit economics with enough clarity. Topgolf added 11 venues last year. What portion of revenue came from those openings versus existing stores? What about revenue contribution from international franchises? How long does it take for a venue to reach maturity? Exactly how many venues are included in your SSS calculation? MODG needs to do a better job communicating with investors.

Simply being more transparent and providing this information could be a catalyst in itself for the stock.

We bought $6500 at $19.38 a share. I would love to buy more, but the high leverage, consumer sensitivity, and lack of disclosure around TopGolf force me to pause. I will buy more, and at higher prices, if MODG can continue to deleverage, TopGolf shows profitability and cash flow, or there’s better unit economic disclosure.