Caesars Entertainment Writeup (CZR)

The House Always Wins.

Thesis:

Caesars Entertainment is a best-in-class casino operator that’s poised to take long-term market share in the digital space, given its comprehensive omnichannel capabilities. Furthermore, the recent completion of a major investment cycle will lead to enhanced free cash flow generation. I believe shares could easily double over the next three years.

Business Overview/History:

In its current form, Caesar’s Entertainment is the Frankenstein baby of private equity and Carl Icahn’s activism. After a massive LBO followed by a messy bankruptcy, Caesars remerged as a public company in 2014. In 2019, Carl Icahn bought a ~10% stake in the company and acquired 3 board seats. As part of his activism campaign, he pushed for Caesars to sell themselves. Caesars would later be acquired by El Dorado Resorts that same year. As part of the deal, El-Dorado acquired all of Caesar’s assets but rebranded themselves under Caesar’s name, given the company’s iconic status. Before the deal, El-Dorado had been rolling up the casino industry with acquisitions of MTR Gaming in 2013, the Isle of Capri in 2017, and Tropicana Entertainment in 2018.

Today, Caesars Entertainment is the largest domestic casino operator in the United States. The company owns and operates 51 casinos, 9 of which are in Las Vegas. 40% of revenue comes from this Vegas Segment, and 52% from its Regional segment(non-Vegas properties). In 2021, Caesars entered online gambling by purchasing William Hill’s US online sportsbook. Today, digital gambling represents ~8% of total sales.

Omnichannel advantage

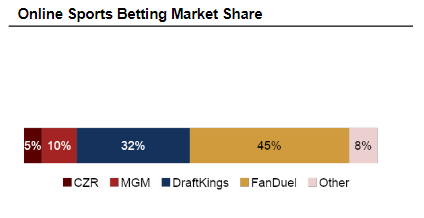

Since the Supreme Court opened the path toward legal sports betting, online sports betting and other forms of digital gambling have exploded in the United States. Today, 38 states have legalized online gambling or sports betting in some form. Handle (the total amount wagered) has grown at an 83.7% CAGR since the 2018 ruling, hitting $90B in 2022. At the same time, advertising and marketing spend by online operators has exploded since legalization. Casinos spent over $1.9 billion on marketing and promotions in 2023! If you’ve watched any live sporting event in the past two years, it’s impossible almost to go a commercial break without one of these ads coming up. As the dust begins to settle in this new market, four dominant players have emerged:

Unlike Caesars and MGM, DraftKings and FanDuel are two pure digital operators. Neither operator has any physical presence in the United States. I believe this is a significant competitive disadvantage for DraftKings and FanDuel going forward.

Unlike Fanduel and DraftKings, MGM and Caesar’s can leverage their physical presence to attract more customers toward their digital products. More specifically, land-based operators can utilize their rewards-member program to drive customers toward their digital offerings. When you currently place a bet in Caesar’s app, you earn Caesar Reward Points based on the size and type of bet. These reward points can then be redeemed for free drinks, meals, hotel rooms, and shows at Caesars’ properties. As a result, Caesars’ online sportsbook users are highly incentivized to visit a property nearby after placing just a few bets.

Furthermore, customers will gamble more upon receiving these rewards, under the illusion they’re breaking even or coming out ahead with the free comps. When in reality, there are no or very little incremental costs for Caesar to provide these freebies. As the customer continues to gamble more, they rack up more reward points for future stays and visits. Caesar’s and MGM’s omnichannel offering between their digital and physical products creates a powerful flywheel for these companies, and thus a competitive advantage over pure digital players.

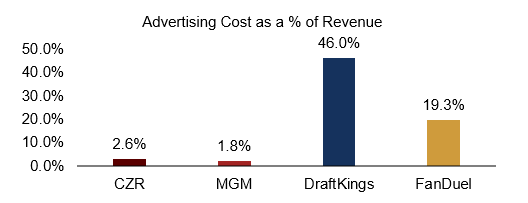

Online operators, on the other hand, must pour more money into advertising and generous promos than their land-based competitors:

But this will eventually create problems as Fanduel and DraftKings transition toward profitability. As these platforms cut back on their generous ad and promo spend, they will lose customers to omnichannel competitors. The loss in market share will diminish growth and can only be reversed by increasing marketing spend again, thus creating a vicious money-losing cycle for Fanduel and DraftKings.

Caesar’s is the best positioned to leverage their omnichannel capabilities, given their 51 physical properties and 65M rewards members. On their Q3 2022 call, management disclosed that cross-over spending (physical spending from customers sourced through the digital app) was already $300m, growing 50% YoY. These omnichannel customers have 3x the lifetime value of pure digital ones. Management has not disclosed omnichannel spending since this quarter for competitive reasons. If we assume omnichannel spending decelerated to 30% growth in FY23, it's not unrealistic to believe cross-over spending approached ~$400M in FY23, or ~4% of total sales.

Outside of omnichannel spending, Caesar has ambitious financial targets for its digital segment on a standalone basis. Upon releasing Caesar’s online sportsbook, management expected to generate 50% cash-on-cash returns at maturity–or about $500M in annual EBITDA. But these great returns came at an immense cost: ~$1.5B in cumulative losses before achieving profitability. And Caesar’s did exactly that. Since launching the app in Q3 21, the digital segment has cumulatively lost $1.1B. Over the past two quarters, The digital segment has been profitable on an EBITDA basis. Management expects the digital segment to earn $500M in EBITDA by FY25. While I find this goal a little lofty, it’s not impossible. Incremental operational changes, like getting hold % in line with other digital operators and renegotiating partnerships with sports leagues, could significantly bolster profitability.

Furthermore, other digital operators have begun demonstrating more rationality around marketing and promotion spend:

“As you can see, we are bringing down promotional reinvestment within states over time. In addition to the natural improvement in promotional reinvestment, we have been deploying multiple initiatives to surgically reduce promotional reinvestment.”-DKNG CFO, November 2023 Investor Day

If other major digital players begin to reduce ad spend, Caesars will have to invest less in marketing and other promotional activities, further boosting profitability.

End of an Investment Cycle

Caesar has spent over $2.5B on capital expenditures over the last three years. Much of this spending was devoted to building and opening new properties, like Harrah’s New Orleans or Caesar’s Virginia. Caesars also renovated and updated all 20,000+ rooms under their management. Throw in a couple hundred million toward building Caesar’s digital capabilities and you have the biggest investment spree in Caesars/El Dorado’s history:

With Caesar’s set to spend another $800M in FY23, management has already signaled that this will be the apex for the foreseeable future:

“CapEx spend is also expected to crest in 2023 at just over $800 million with several growth projects being completed either later this year or in 2024. Coupling declining interest expense and CapEx with continued EBITDA growth sets up for accelerating free cash flow dynamics going forward.” -Brett Yunker, Caesars CFO, Q2 2023 Earnings call

Management has also committed to not having any massive new casino projects in the future:

“There are some meaningful projects in particular markets, but you're not looking at the $300 million, $400 million, $500 million capital outlays.” -Tom Reeg, Caesars CEO, Q2 2023 Earnings Call

Caesars will have significantly more free cash flow with these reductions in capital expenditures. What will management do with all this excess cash? History tells us more gaming M&A. However management has expressed some hesitancy about properly executing this strategy:

“Short answer is no. I won't give you except maybe we'll buy Stifel. Steve, it's you know who's out there. You know what's possible. You know that there are -- at our size, it's not as easy to find targets that, a, move the needle and, b, are actionable from an antitrust perspective, but there's not 0 targets available out there. And as we get to the free cash flow levels that we get to, given what we have generated in the past in terms of returns, it shouldn't be surprising to anybody that we're going to look for opportunity to keep doing that again.”-Tom Reeg, Caesar CEO, Q2 2023 Earnings Call

Now Tom Reeg and the El Dorado team have a great track of creating shareholder value through M&A. But with the universe of targets now smaller, management could turn inward with capital allocation. At only 8x forward EBITDA, Caesar’s stock is not expensive. And Reeg is definitely smart enough to recognize its value, given his prior experience in investment management/sell-side research.

With capital expenditures set to decline, I estimate Caesars could do $2B in levered free cash flow in FY25. Even if it spent just half that doing share buybacks, management could still retire ~10% of the float in a year.1

Management:

Caesars Entertainment is led by CEO Thomas Reeg, who is widely regarded as one of the best operators in the gaming industry. Since being promoted to President of North America in 2014, Reeg was instrumental in executing El Dorado’s roll-up strategy. During that time, El Dorado stock has more than 10x under his leadership.

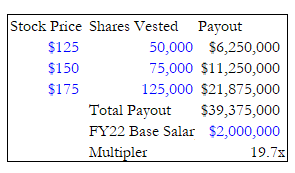

Upon completion of the William Hill Acquisition in 2022, Reeg received a radically overhauled incentive package. He was given over 250,000 shares in performance equity options that don’t begin vesting until $125 a share. Below is a payout chart of these options:

Now these options expire in February of 2025. Caesar’s current stock price is ~$43. Will Reeg be able to cash any of these options in the money? Probably not. But is this potential massive payout nagging him in the back of his mind? Absolutely. 2024 is the last full year these options are outstanding, and I think Reeg will do everything he can to get them in the black. Whether that’s through massive deleveraging or capital returns remains to be seen. But this is an incrementally positive dynamic for the stock in the short term.

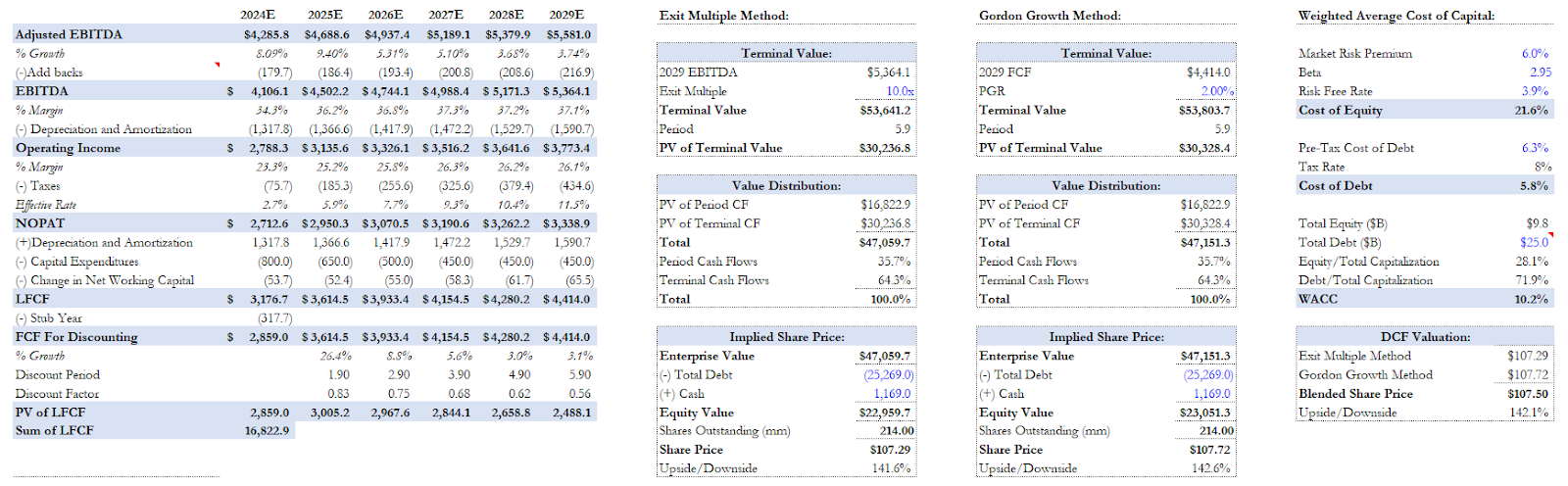

Reverse DCF:

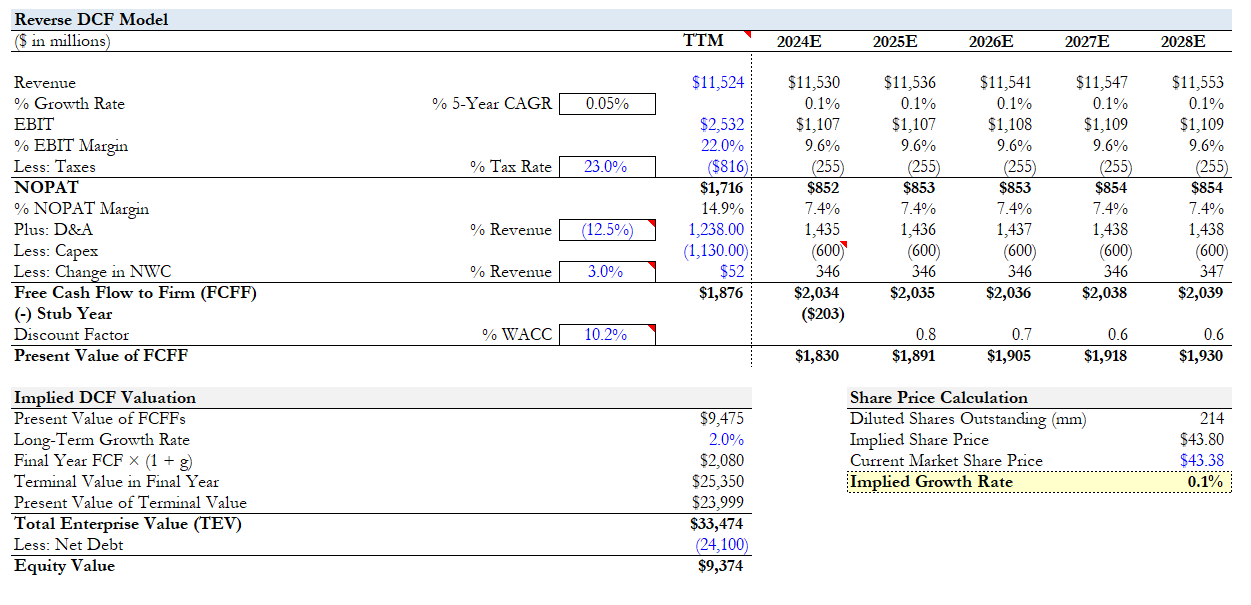

As part of my analysis, I created a reverse DCF to figure out the fundamental expectations embedded in Caesar’s current stock price. For simplicity, I modeled out D&A and working capital movements based on historical performance. I also used the same PGR (2%) and WACC (10.2%) from my actual DCF. Using these inputs, I found that the market is pricing in essentially no growth and significant margin degradation going forward:

These are very punitive expectations tied to Caesar’s business. Why are investors so skeptical about Caesars?

I believe Caesar’s leverage and prior insolvencies have scarred investors from the name. Currently, Caesar is running at ~3.25 leverage (Debt/EBITDA). This calculation, however, excludes operating leases. If you include those obligations, then Caesar’s is currently running at over 6x leverage.2 When you consider Caesar’s leverage in the context of their messy bankruptcy in 2015, you can understand why investors might be hesitant about investing.

But this is precisely where the opportunity lies. Management has demonstrated its commitment to deleveraging, by reducing debt by $1B a year. The Federal Reserve lowering interest rates in 2024 also makes refinancing cheaper going forward. Furthermore, unless the consumer gets hit by a meteorite, like in Q1/Q2 2020, there’s no plausible scenario where Caesar’s is insolvent or has to raise equity.

Caesar’s stock setup reminds me a lot of Garrett Motion two years ago: A good business weighed down by investor pessimism over a prior bankruptcy that is highly unlikely to repeat. And that setup has worked out quite well for us!

Valuation:

For my base case, my core fundamental assumptions are:

Vegas Segment: I model out Vegas revenue growing at 3.3% CAGR over the next five years, driven by an uptick in gambling due to Caesar’s omnichannel offering. Adjusted EBITDA margins also expand 150 basis points to 48.5% by FY29.

Regional Segment: Revenue grows at a 2.2% CAGR through FY29 with Adjusted EBITDA margins expanding to 37% over that same period.

Digital Segment: Revenue will grow at a 16% CAGR over the next five years with an inflection toward full-year profitability as soon as this year. EBITDA Margins then expand from 12% in FY24 to 25% in FY26, then reaching a steady state of 30% by FY29

Capex: Capital expenditures peak in 2024 at $800m with the completion of Harrah’s Virginia and Caesar’s New Orleans property. Spending then declines by $150M a year in FY25 and FY26, before approximating Caesar’s maintenance capital expenditure of $400-$500M a year.

Plugging these assumptions into a DCF, along with a 2% terminal growth rate and 10.2% WACC, I value Caesars at $107 a share, or 141% upside.

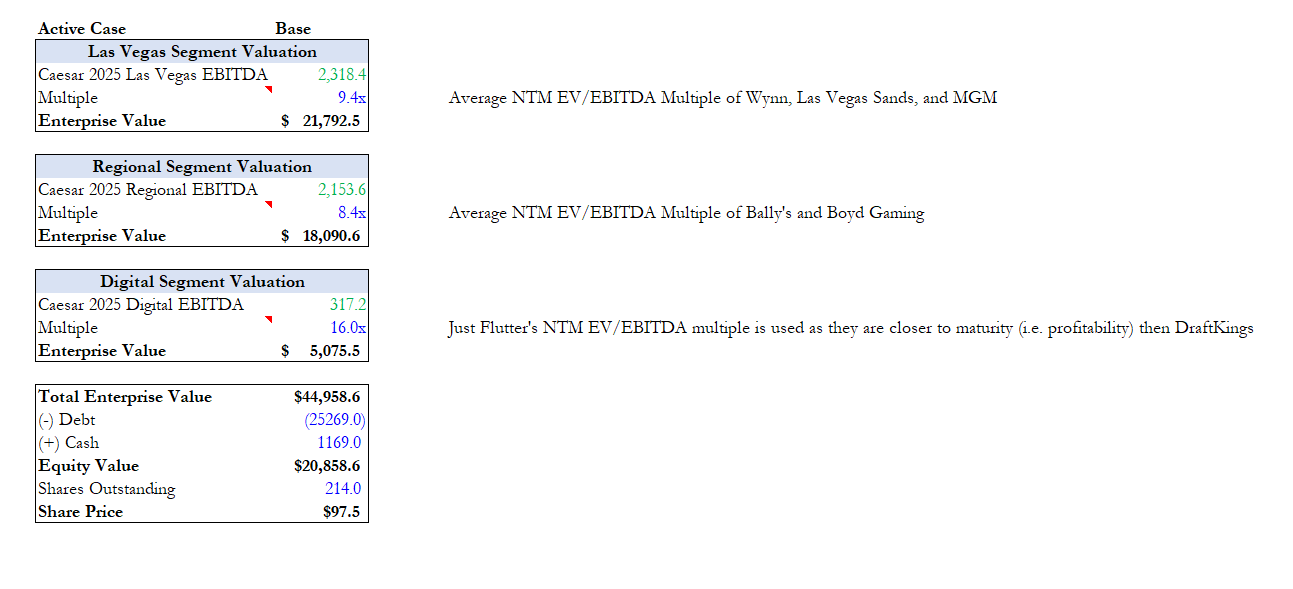

I also did a Sum of Parts analysis, valuing Caesars’ Vegas, Regional, and Digital segments separately with my 2025 EBITDA estimates:

This analysis yields a target price of $97.5 a share.

Risks:

Recession: Like other consumer discretionary names, Caesar is sensitive to any economic downturn.

Leverage: On a traditional basis (Debt/EBITDA), Caesar is currently running ~3.25x leverage. Including operating leases, that leverage shoots up to ~6.5x. As mentioned above, I believe much of the skepticism around Caesars relates to its indebtedness and prior insolvency. Management, however, is committed to reducing leverage as fast as possible, to the tune of $1B+ in annual debt reduction. Furthermore, The Federal Reserve’s recent signal to lower interest rates will also make refinancing easier for Caesar’s going forward.

Digital Profitability: Some investors are skeptical that digital casinos will ever be as profitable as traditional land-based casinos. Online operators in Europe, which legalized online gambling many years ago, are immensely profitable with 25%+ EBITDA. There is no structural reason for why American online operators should be any less profitable at maturity.

Legislative: Despite appearing like a secular trend, gambling legalization and regulation have historically been quite cyclical. Legalization is typically succeeded by more stringent regulations and oversight in the years that follow. The UK, which legalized online gambling years before the US, has already followed this pattern.

We are going to buy $7500 worth of shares today, with plans to add more if any capital returns are announced or digital profitability is confirmed. We are going to sell completely out of our top golf position to fund most of this position.

We sold all of our TopGolf positions for ~$13.24 a share (32% loss). The other half of the trade ($3100) was funded with our cash position. We bought 175 shares at $42.93.

Assuming an Average Share Price of $50.

Should operating leases be considered debt? According to some accountants, yes. According to others, no. But for conservatism, I considered these obligations as debt in my valuation.